Are We Nearing an Inflection Point?

Topic of the week:

This week we’ll look at the state of the economy from the lens of commodities, as well as public materials companies, which historically have had some compelling evidence as potentially leading indicators of the broader economy.

But before we do, we’d like to share with you what we’ve been reading lately from our fellow investing writers here on Substack - the Money Machine Newsletter:

/ X")

8,000+ investors start their week with Money Machine Newsletter's insights to get smarter about investing in stocks. It's free, it's fast, it's a no brainer—just your weekly dose of market-beating stocks in a 5-minute read.

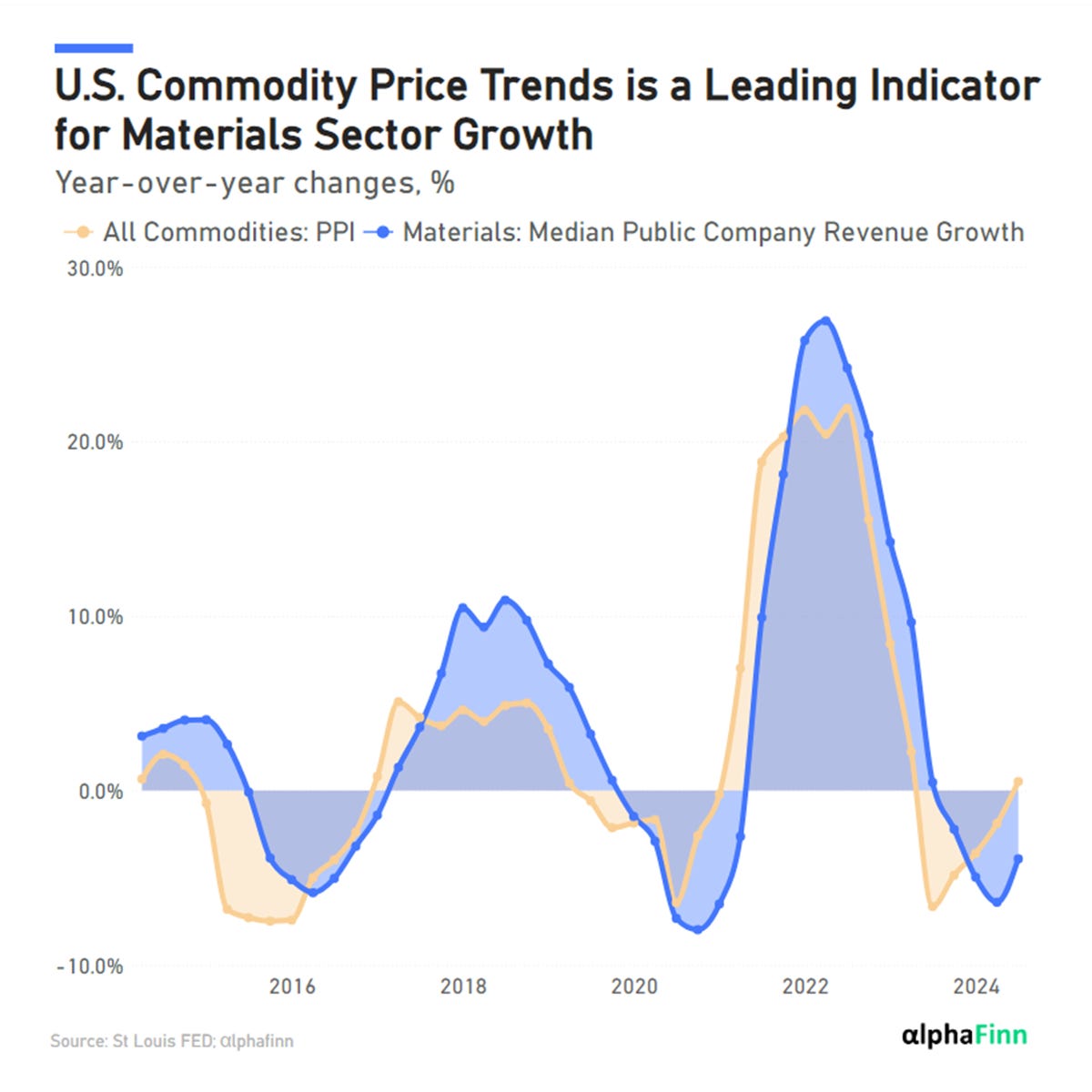

Commodity Prices and Revenue Growth: Are We Nearing an Inflection Point?

Over the past decade, U.S. commodity price movements have served as a leading indicator for top-line growth in the Materials sector. The Materials sector is sensitive to commodity price volatility, and historically, it has provided valuable insights into the broader economic cycle.

Today, we’re once again seeing potential signs that suggest the economic slowdown could persist for longer.

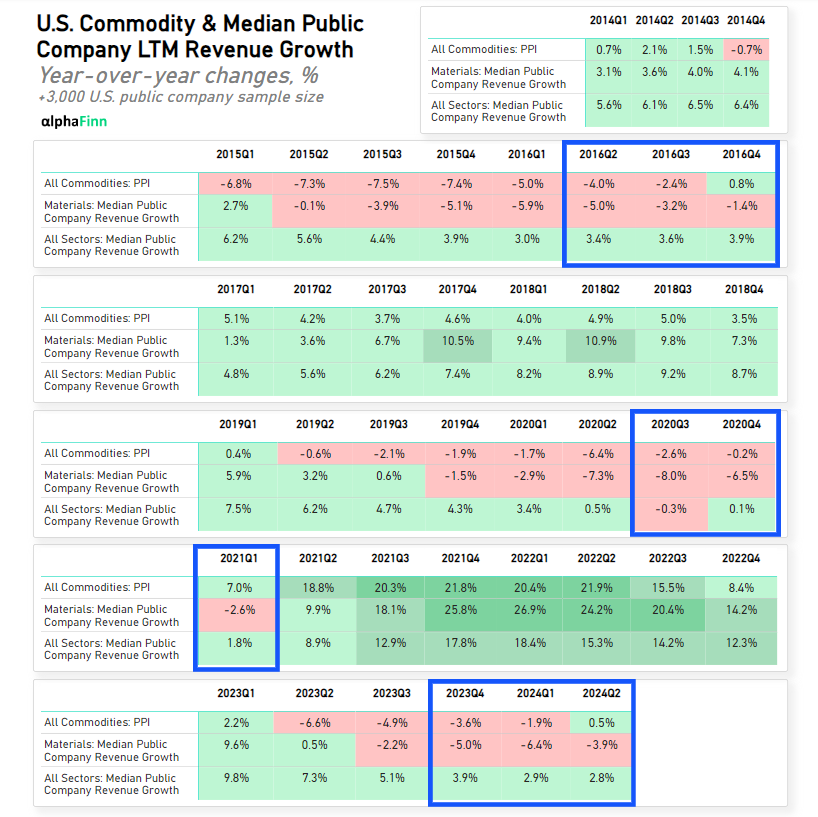

95% correlation between year-over-year changes in: i) All Commodities PPI; and ii) Median revenue growth of Materials sector public companies, with commodities leading by one quarter, based on data from the past 10 years.

In the past 10 years, the sector has experienced three periods of negative revenue growth, each lasting at least four consecutive quarters and coinciding with broader slowdowns in both U.S. real GDP and median public company revenue growth.

Before recovering from the past two growth downturns, three signals were prevalent both times:

1️⃣ Revenue declines in Materials began to reduce over two consecutive quarters.

2️⃣ Broader market revenue growth improved for at least two consecutive quarters.

3️⃣ Commodity prices shifted from negative to positive momentum.

Where Do We Stand Today? Can Any of the Above Boxes be Checked?

(✅/❌) Materials revenue has improved compared to the previous quarter, but it's been just one quarter yet.

(❌) Broader U.S. public company revenue growth continued to contract last quarter.

(✅) Commodity prices have turned positive.

So what?

While it’s still early, if history is a guide, we could be 1 to 3 quarters away from a broader expansionary phase.

As the saying goes, history doesn’t repeat itself, but it often rhymes.

Transition.

If you’d like to access the data used above, and much more financial & macroeconomic figures, including over 3,000 U.S. listed stocks… well, you can! Check out αlphaFinn below, offering a 7-day FREE trial for new users.